Will the bull market endure or fizzle out?

Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

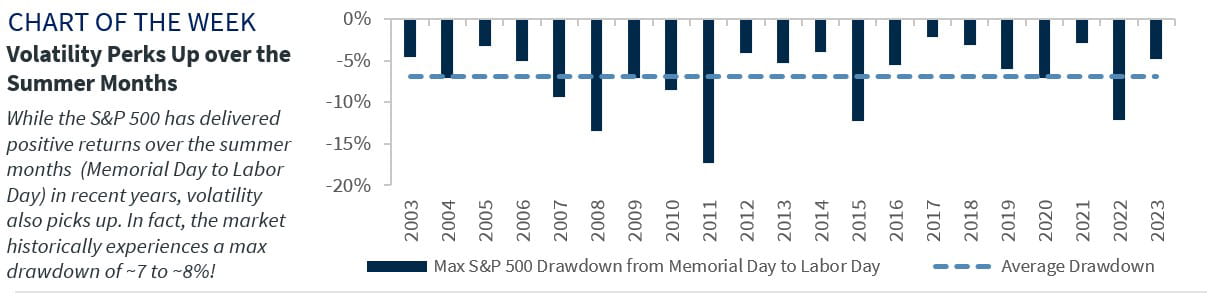

- Volatility Perks Up in the Summer Months

- Technicals Suggest the Equity Market is Stretched

- Long-Term Fundamentals Remain Supportive

Happy National Flag Day! While Flag Day is not a federal holiday, this observance day gives patriotic Americans another day to celebrate the red, white and blue! The origins of Flag Day date back to 1777, when Congress first approved the design of our national flag. Since the nation’s founding, there have been 27 different versions of the flag. The original outline, with its thirteen alternating red and white stripes and the blue canton, remains intact. And speaking of the number 27, the S&P 500 surpassed its 27th record high for the year this week—and still notching more (up to 29 already!)—driven by rising earnings, cooling inflation, and an economy that remains on solid ground. With the S&P 500 crossing 5,400 for the first time ever, we discuss whether the 20-month long bull market rally will endure or fizzle out.

- A Short-Term Pullback May Be In The ‘Stars’ | After a sharp and steady rally from its October 2022 lows, it’s normal to question how much more upside the S&P 500 has from current levels—particularly given it is 4% above our year-end 5,200 target. While we remain bullish longer term, the market could trade sideways or lower in the months ahead for the following reasons:

- Volatility Perks Up In The Summer—‘Sell In May And Go Away’ is a popular Wall Street adage even though it has not worked in recent years. Case in point: the S&P 500 has been positive during the Memorial Day to Labor Day period in 7 out of the last 8 years. But despite this positive overall performance, stocks have historically suffered an average drawdown of ~7% at some point during the summer. And given that 2024 is an election year, uncertainty and volatility are likely to pick up again. In fact, if the historical pattern holds, the normal seasonal volatility could temporarily drive the S&P 500 back toward 5,000.

- Stretched Technicals—Near-term technicals suggest that the current rally is stretched. The 14-day RSI (relative strength index) rose into overbought territory (a level >70), with MAGMAN* (the main driver of the S&P 500’s returns) even more stretched at an RSI of 84. The S&P 500 is also ~13% above its 200-day moving average—a level that has historically led to some near-term consolidation. Finally, investor sentiment is getting euphoric—as seen in the % of investors expecting stock prices to move higher over the next 12 months climbing to the third highest level over the last 30 years and strategists racing to raise their targets given the recent rally. These factors suggest the equity market may be due for a period of consolidation.

- Economic Data Remains Murky—Recent economic data has provided conflicting signals (weak retail sales, strong jobs report), making it challenging for policymakers to have confidence in the underlying trends. However, with the Fed in no hurry to cut rates and its monetary policy stance restrictive, every upcoming data release will be critically important. While a soft, non-recessionary landing remains our base case, any signs of a faster than anticipated slowing in the labor market or an abrupt pullback in consumer spending could spell trouble for equities given the economic impact on earnings. Next week’s read on retail sales will be key, particularly given the softening consumer demand flagged in 1Q earnings reports.

- Longer Term, Fundamentals Earning Their ‘Stripes’ | While some near-term consolidation is likely, the longer-term forces remain in place for the continuance of this bull market. Here’s why:

- Falling Rates Will Be A Tailwind—Stocks should benefit from a powerful tailwind once the Fed pivots to rate cuts—particularly if policymakers are successful in delivering a soft landing. After a series of setbacks earlier in the year, recent inflation readings (PCE, CPI, and PPI) have improved. While the Fed is playing it safe, waiting for more good data, rate cuts are still on the horizon. Once the Fed begins to cut rates, this will support multiples (P/E ratios move inversely with rates), entice investors out of cash into risk assets, like equities, and drive interest rates lower—making equities relatively more attractive.

- Earnings Remain Supportive—Over the longer term, earnings are the primary driver of market returns. And, earnings trends have been positive this year. In fact, 2024 earnings estimated have climbed ~1% since the start of the year (typically they are revised down 2-3% at this juncture) and are on pace to rise 12% YoY. We expect forward earnings to move higher with further investment in AI (supporting the Tech-sector earnings—the largest weight in the S&P 500), a focus on cost cutting from businesses (to defend margins, which remain above historical averages), and lagged impact from fiscal spending packages.

- Gains Should Spread To Other Sectors—This week marked two milestones for the current bull market—it is now up over 50% since it began, and it has lasted 20 months. Despite these milestones, history suggests that the current bull market is not finished. While the 52% return may seem like a strong return, it is worth noting that it is below the average ~60% return of a bull market at this juncture. Additionally, only two sectors (Info Tech and Communication Services) have outperformed the broader market over that time period, which points to our expectation that there is room for performance to broaden out. As the median bull market is up 114% and lasts for ~five years, this suggests that the bull market still has room to run.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.